Version of this article appeared in Advisor Perspectives on December 13, 2021.

Helping a client reach their financial goals while managing risk is the most fundamental part of an investment advisor’s job. While we can all agree that rebalancing is key to doing it well, there is almost no universal agreement on the best way to approach the process.

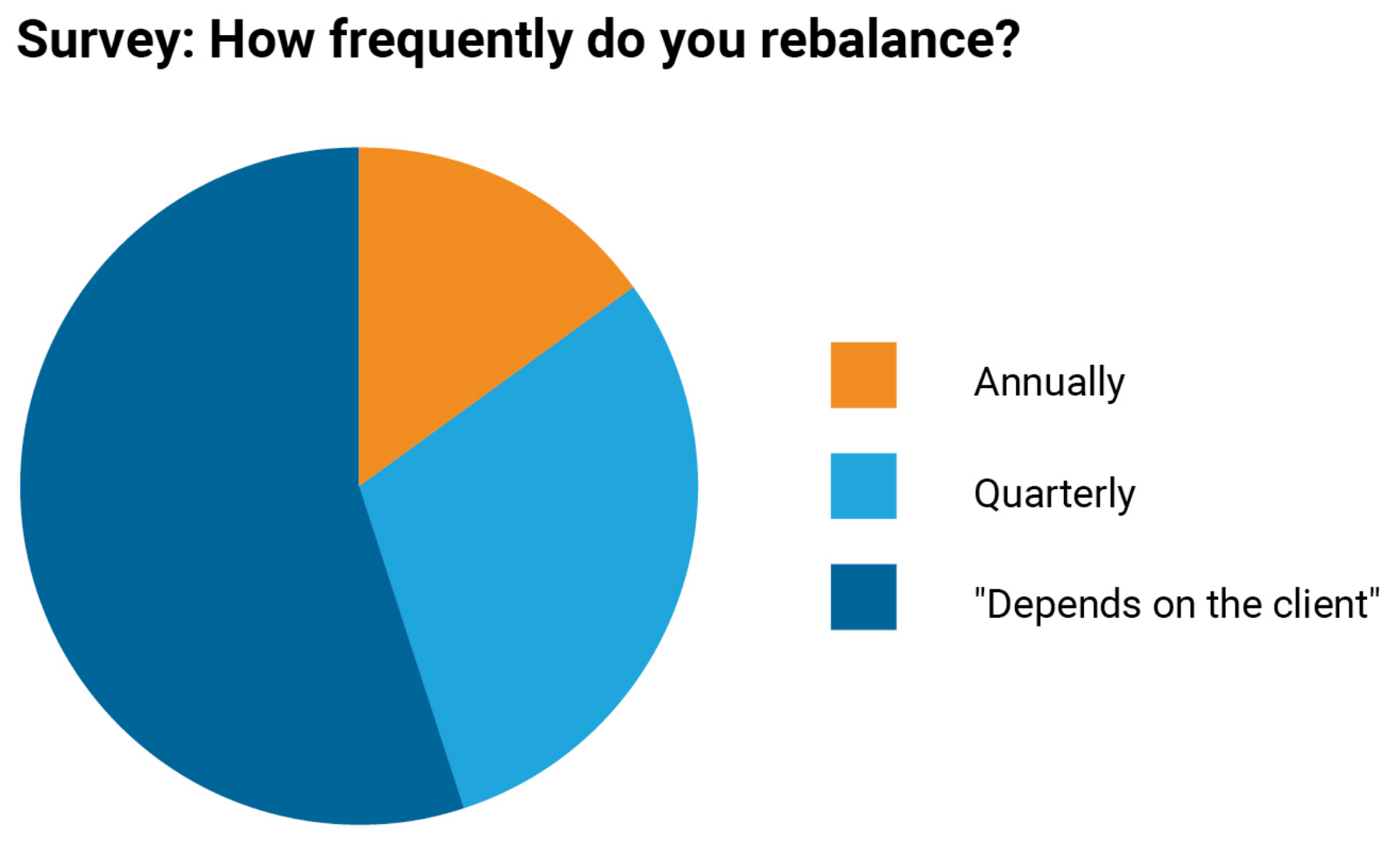

Each year in Advyzon’s annual survey, we ask the advisory firms we work with a series of questions regarding their firm and their practices. This year, we asked advisors how frequently they rebalance, which yielded interesting results.

Out of 300 respondents, roughly 30% said they rebalance quarterly, about 15% said annually, and the remaining 55% said, “Depends on the client.” We weren’t surprised that so many said it depends on the client, but we wanted to understand what that might mean in practice. In this article, we cover the most popular approaches to managing the rebalancing frequency for your firm. This might help you feel confident in your own approach or give you new ideas.

The case for quarterly rebalancing

The biggest arguments in support of quarterly rebalancing are market volatility and/or major bull (or bear) markets. In these cases, allocations can shift off target in a relatively short period of time. A quarterly rebalance gives you the ability to maintain the allocation that is appropriate for your client. Waiting to rebalance annually could leave your clients with a portfolio that doesn’t match their risk tolerance.

Since most advisors bill quarterly, timing your rebalancing to sync with your reporting and billing cycle is another potential benefit to this approach. It also creates a natural opportunity for discussing any adjustments with clients.

The case for annual rebalancing

In some circumstances, annual rebalancing may be just as good as quarterly rebalancing at managing risk while also striving for the best possible returns. This is especially true when you take potential transaction costs and tax implications into account.

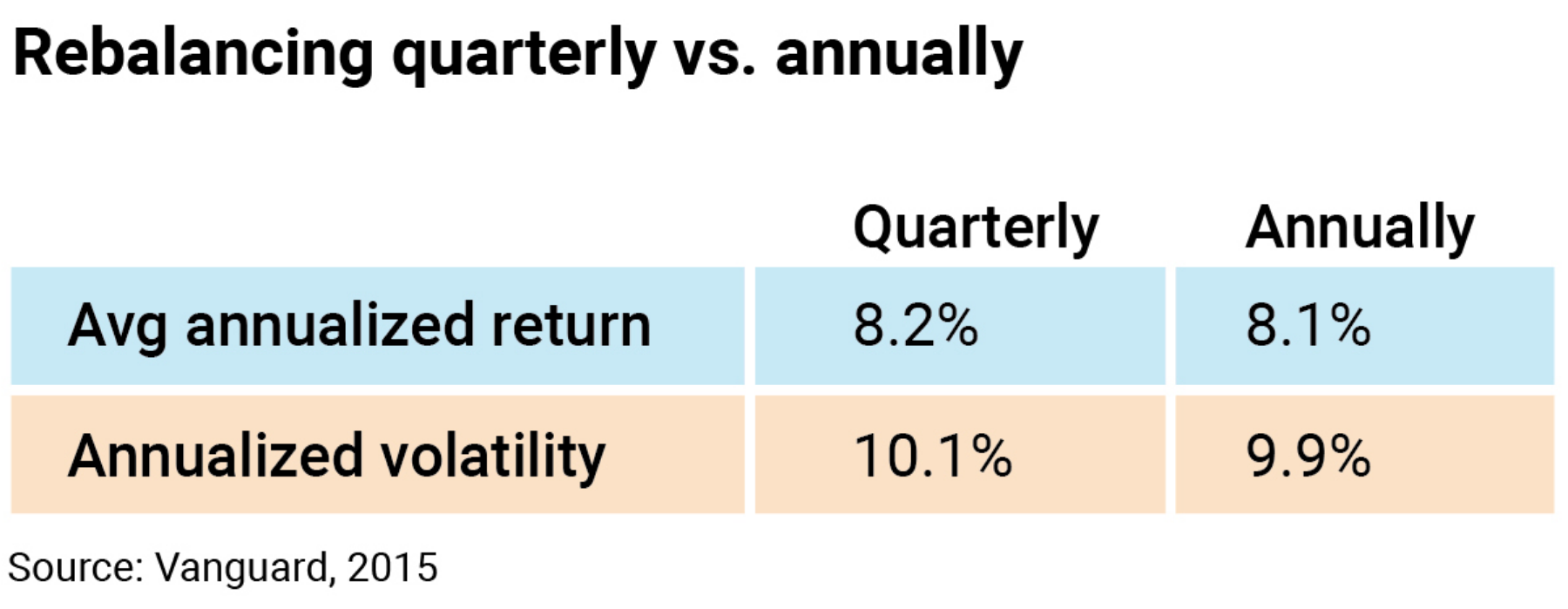

According to a Vanguard study on rebalancing conducted in 2015 and going back to 1926, there was no material difference between quarterly and annual rebalancing, and rebalancing annually came with marginally lower volatility. Timing and market cycles are definitely at play in this analysis as rebalancing too frequently could mean selling out of a bull-run or compounding losses in a bear market.

The case for threshold rebalancing

Some advisors might argue that time-based rebalancing is the wrong approach; they might favor threshold rebalancing instead. In this scenario, an advisor would rebalance a client portfolio when the asset allocation moves far enough away from its target (or reaches a threshold). For a 50-50 portfolio, this might happen when the portfolio hits 60-40. If the threshold is never breached — say equities outperform but pull back before the threshold — the advisor would simply hold, thereby minimizing transaction costs and potential tax issues.

There are a few things to consider before deciding to use threshold rebalancing. First, you may need to take more care to explain this process to clients, as it can be less intuitive than the idea of rebalancing on a schedule. Second, you’ll need to figure out the appropriate threshold. Unlike time-based rebalancing, which is triggered regardless of the portfolio’s makeup, the thresholds that make sense are likely to vary based on the number of assets held. For example, a 10% threshold wouldn’t make sense in a portfolio with five asset classes.

CPPI rebalancing

Constant-Proportion Portfolio Insurance (CPPI) is a fancy name for a simple concept: The more wealth you build, the greater your presumed risk tolerance. Under this assumption, as a client builds assets, a greater proportion of their portfolio could be devoted to riskier investments, such as stocks. There are prescribed formulas you can use to calculate the target percentage for equities using this approach.

It’s also worth considering a client’s risk appetite in addition to their risk tolerance. When it comes to how clients will perceive your advice and your performance, it’s important to look beyond what their portfolio can withstand. You must also meet their expectations around risk.

Regardless of the approach to rebalancing you use, it’s important to have a system you trust to create, review, and execute trades, and communicate any updates with clients. That’s why Advyzon decided to build our own rebalancer. We wanted to make sure our tools integrated seamlessly with the rest of the Advyzon platform. Quantum has been in beta-testing for much of 2021 with 20+ advisors to ensure everything works properly. Expect to see it widely available to Advyzon clients in 2022.